Including a U.S. vs. China Comparison + Company Profiles (NVIDIA, Hyundai, Robotics Makers)

Introduction:

In 2026, the next frontier of AI is not merely virtual — it is Physical AI, where artificial intelligence intersects with real-world environments via sensors, semiconductors, and autonomous machines. This phenomenon spans robotics, autonomous vehicles, smart factories, and embedded AI systems — and it is rapidly becoming a strategic battleground for U.S. and Chinese technology leadership.

Physical AI is reshaping the entire deep tech value chain — from foundational hardware like GPUs and ASICs, through software frameworks and simulation, to mechanical robotics and end-user applications in manufacturing, mobility, and services. This post synthesizes the key segments, compares major U.S. and Chinese players, and identifies strategic investment angles for 2026 and beyond.

What is Physical AI?

Physical AI refers to AI systems that perceive, reason, plan, and act in the physical world by combining real-time sensory data with adaptive decision-making. Unlike traditional software-only AI, Physical AI must fuse hardware (sensors, chips, actuators) and software (ML models, simulators, control frameworks) into systems capable of interacting with their environment autonomously.

Key domains include:

- Robotics: Humanoid and non-humanoid mobile robots

- Autonomous Mobility: Cars, delivery drones, AGVs

- Smart Manufacturing: Digital twins and AI-powered factories

- Embedded Systems: AI at the edge in hardware devices

In essence, Physical AI is where software “meets” the physical world — and large swaths of future industrial growth hinge on mastering this convergence.

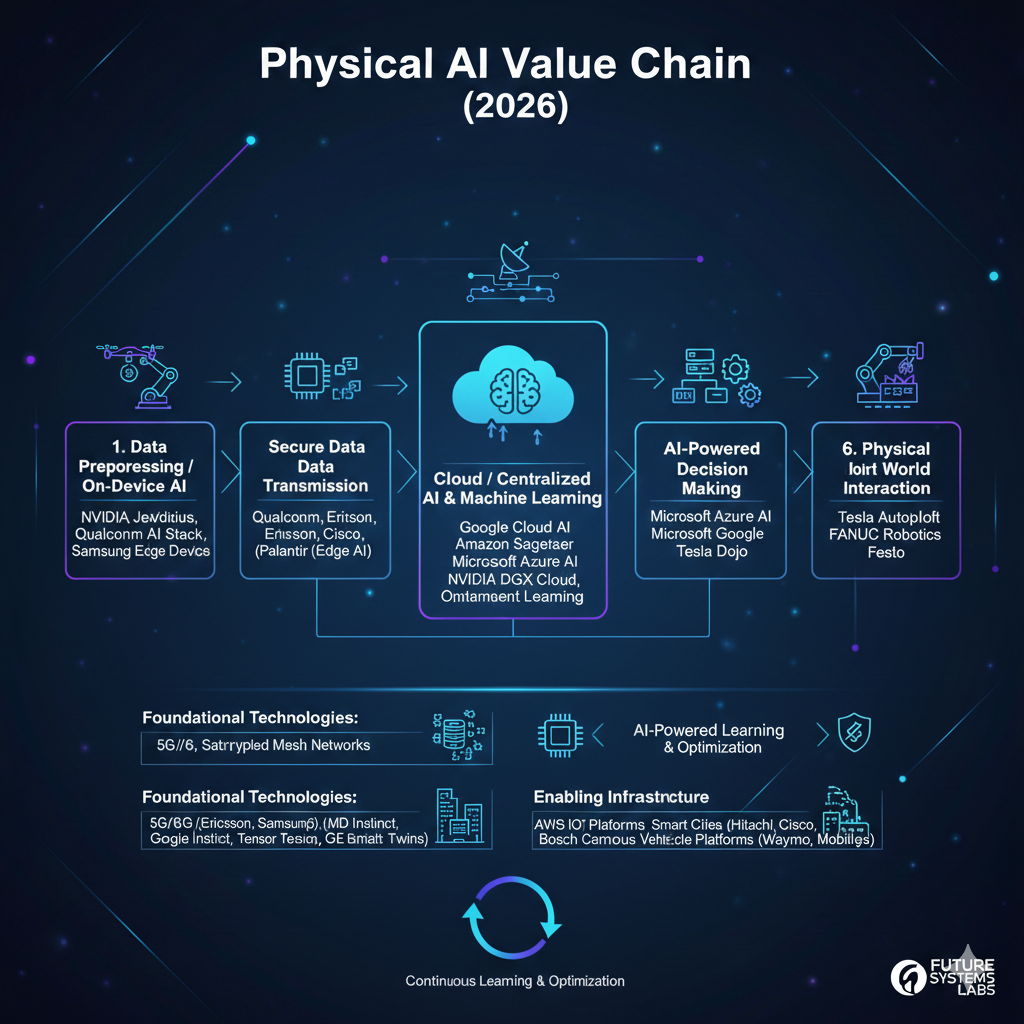

The Physical AI Value Chain – Layer by Layer

🧠 1. Foundational Compute & Hardware

This layer provides the raw computational horsepower necessary for running AI workloads and real-time decision-making.

| AI Accelerators (GPUs/ASICs) | NVIDIA, TSMC (manufacturing), Samsung, Intel | NVIDIA Blackwell GPU series is a cornerstone of Physical AI compute, used for training and inference in robots and factories. |

| Edge AI Modules | NVIDIA Jetson, Qualcomm, MediaTek, Intel RealSense | Edge modules provide inference close to sensors — crucial for real-time control in robots and vehicles. NVIDIA Jetson Thor targets industrial/robot deployments. |

| Sensors & Perception | RealSense (Intel spin-out), Lidar makers, IMUs | High-accuracy sensors are the “eyes and ears” of Physical AI systems. RealSense depth cameras are widespread in autonomous robots. |

Investment Insight:

Compute platforms (especially GPUs tied to NVIDIA’s ecosystem) are the foundation — but constraints on advanced chips (especially in China) make supply chain diversification and foundry partnerships (TSMC, Samsung) strategically critical.

🧩 2. Software Infrastructure (AI Models & Development Platforms)

Software drives autonomy and learning.

| AI Foundation Models + Physical AI Models | NVIDIA Cosmos, GR00T models | NVIDIA is releasing open Physical AI foundational and world reasoning models. |

| Simulation & Digital Twin | Omniverse, Isaac Sim | Used for training and validating robots in virtual environments before deployment. |

| Robot Operating Frameworks | CUDA, ROS, custom middleware | Ecosystem enablers that integrate perception, control, safety |

Investment Insight:

Software platforms are the glue of Physical AI. NVIDIA’s open models and integrated frameworks significantly lower development barriers, making it both a platform play and an enabler of third-party growth.

⚙️ 3. Mechanical & System Integration (Robotics Hardware)

Robotics hardware translates brain into body — the physical outputs.

| Humanoid Robots | Boston Dynamics Atlas (USA/Korea) | U.S./Korea |

| Quadrupeds & AMRs | Unitree, ANYbotics | China/Europe |

| Industrial Arms & Cobots | Fanuc, ABB, Yaskawa | Global |

Notable systems and approaches:

- Atlas (Hyundai / Boston Dynamics) — production-ready humanoid robot for industrial tasks.

- Unitree Robotics (China) — mass-market quadrupeds & humanoids at lower price points.

- UBtech (China) — humanoid robots for industrial/logistics use.

Investment Insight:

Hardware is costly and complex — but Chinese players are aggressively scaling, often at much lower unit costs, creating global competitive pressure.

📦 4. Applications & Services

This layer includes use cases where Physical AI generates revenue:

- Smart factories and digital twin deployment

- Autonomous logistics and warehouse robotics

- Healthcare and hospitality service robots

- Mobility (autonomous vehicles + driver assistance)

Funding and deployments in this layer often reveal which parts of the value chain are monetizable fastest.

U.S. vs. China – Strategic Comparison

🇺🇸 United States – Platform and AI Stack Strength

Strengths

- AI compute leadership: NVIDIA’s GPUs and software ecosystem remain the foundation for robotics and Physical AI development.

- Rich software ecosystem: Strong middleware, simulation tools, and open-source platforms.

- High-end robotics R&D: Boston Dynamics leads in sophisticated mechanical design.

Challenges

- Higher hardware cost compared to Chinese counterparts.

- Production scaling remains slower due to labor and manufacturing costs.

🇨🇳 China – Scalability and Deployment Focus

Strengths

- Rapid scaling of robot production (quadrupeds & humanoids) with price competitiveness.

- Government backing and funding streamlines commercialization.

- Broad ecosystem of robotics makers across segments.

Challenges

- Chip access limitations due to geopolitical constraints (export controls).

- Perception and autonomy stacks still often dependent on Western software.

Investment Insight:

China’s rapid scaling of robotics hardware — especially at price points far below Western equivalents — could accelerate adoption across industries. However, reliance on non-local compute components may undercut growth if export policies tighten further.

In-Depth Company Profiles

🟠 NVIDIA — The Physical AI Software & Hardware Backbone

NVIDIA is arguably the most pivotal player in the Physical AI ecosystem. Beyond its foundational GPU business, NVIDIA is extending its platform into robotics and autonomous systems:

- AI Compute Infrastructure: Blackwell GPUs power training, simulation, and in-field autonomy.

- Physical AI Models: NVIDIA Cosmos, GR00T and world reasoning models radically simplify building intelligent agents that can perceive and act in physical environments.

- Simulation & Robotics Platforms: The Omniverse and Isaac Sim ecosystems enable developers to create digital twins and simulate complex robotics behaviors before deploying into real world.

- Edge Integration: Jetson platforms bring real-time inference to robot bodies.

- Ecosystem Partnerships: NVIDIA’s stack is used by major U.S. robotics firms like Agility Robotics, Amazon Robotics, Figure AI, and more.

Investment Angle:

NVIDIA sits at the top of the Physical AI value chain as a foundational platform provider. It benefits from both software recurring revenue and the broader ecosystem’s growth, making it uniquely positioned to capture value from almost every segment of this industry.

🔵 Hyundai Motor Group — From Mobility Giant to Physical AI Integrator

Hyundai has articulated a bold strategy to become a Physical AI leader, marrying its automotive expertise with robotics and AI:

- AI Robotics Strategy: At CES 2026, Hyundai unveiled a comprehensive Physical AI roadmap, aiming to integrate robotics, manufacturing processes, autonomous mobility, and real-world AI data.

- End-to-End Value Chain: Hyundai is leveraging its manufacturing scale and affiliates (including Hyundai Mobis, Hyundai Glovis) to build an integrated robotics lifecycle — from development to field service.

- AI Factory with NVIDIA: In partnership with NVIDIA, Hyundai is building an AI Factory equipped with 50,000 Blackwell GPUs aimed at next-generation smart factory, autonomous driving, and robotics innovation.

- Atlas Deployment: Based on Boston Dynamics designs (owned by Hyundai), Hyundai plans to mass-produce up to 30,000 humanoid robots annually by 2028 and deploy them in U.S. factories from 2028 for logistics and assembly tasks.

Investment Angle:

Hyundai’s strategy blends automotive scale + robotics integration — attracting cross-sector capital, and positioning it as one of the few non-U.S. industrial players with a fully integrated Physical AI roadmap.

🤖 Key Robotics Manufacturers & Innovators

🔹 Boston Dynamics (USA / Hyundai)

- Pioneer in advanced legged robots — Spot and Atlas.

- Now integrated with Hyundai’s industrial strategy for real-world robotics.

Investment Angle: A high-end robotics design powerhouse, now scaling via Hyundai’s production capabilities.

🔹 Unitree Robotics (China)

- Offers quadruped robots and emerging humanoids at significantly lower price points.

Investment Angle: Volume play in global robotics hardware — capturing demand in cost-sensitive markets.

🔹 UBtech Robotics (China)

- Specializes in humanoids for logistics, industrial use, and services.

Investment Angle: Positioned for wide adoption across industrial and commercial use cases.

🔹 Figure AI (U.S.) & Other Startups

- Building general-purpose humanoid robots supported by major venture capital and strategic partners including NVIDIA.

Investment Angle: Early-stage value creation if robotics reach mainstream adoption.

Strategic Investment Themes for 2026

🔥 1. Platform Dominance Pays

Invest in companies that control software, compute, and simulation stacks — especially NVIDIA whose ecosystem is indispensable.

🤖 2. Robotics at Scale

Volume manufacturers (Unitree, UBtech) benefit from price elasticity and adoption in commercial deployment — particularly if China accelerates exports.

🧩 3. Embedded AI + Edge Sensors

Companies like RealSense and advanced sensor makers will benefit from Physical AI’s demand for high-fidelity perception hardware.

🏭 4. Integrated Industrial Value Chains

Hyundai and similar conglomerates with production scale and AI capability may unlock sustained margin growth by controlling both hardware output and AI intelligence.

🌍 5. U.S.–China Tech Competition

Trade restrictions and semiconductor policy remain a double-edged sword: benefiting domestic players but potentially stifling global collaboration.

Conclusion

Physical AI is establishing a multi-trillion-dollar value chain — from semiconductors and sensors to software platforms and autonomous machines.

- NVIDIA stands as the software and compute backbone powering innovation across industries.

- Hyundai is transforming from an automaker into a Physical AI integrator with global manufacturing scale.

- Robotics makers in the U.S. and China are redefining how humans and machines collaborate.

For investors, understanding the multilevel nature of this ecosystem — from chips and simulation to robots and real-world deployment — is key to identifying winners in this next technological wave.

'분석' 카테고리의 다른 글

| 2026년 시놀로지(Synology) NAS 선택 가이드: 모델별 비교부터 가격까지 완벽 정리 (3) | 2026.02.01 |

|---|---|

| 2026년 최신 사잇돌 대출 완벽 가이드|자격·금리·한도·신청방법·주의사항 총정리 (0) | 2026.02.01 |

| The Secret Life of Coca-Cola: Unpacking the World's Most Guarded Recipe (0) | 2026.02.01 |

| Navigating the Used PC Parts Bazaar: Your 2026 Price Guide to SSDs, CPUs, RAM & HDDs (0) | 2026.02.01 |

| 三星电子 vs SK海力士 深度解析 (0) | 2026.02.01 |